Pop Quiz – Are U.S. stocks up or down through the first six months of the year? Given the endless stream of recent bad news (European recession, China’s slowing economy, global banking ills, etc.), answering “down” would be understandable. Once again, it feels like all the news is bad, and that the big drivers of the capital markets are forces beyond one’s control and maybe even understanding. Those following closely the gyrations of the capital markets may feel that economic and stock market cycles have grown shorter in duration and more pronounced in fluctuations. Those who follow the markets less closely probably feel a discomforting sense that something is wrong – with the markets, the economy, the government, or all of the above. A palpable malaise has settled over the retail investor (as evidenced by recent sentiment surveys) just like the brown smog covering Los Angeles in a 1980s movie. If the reader does not feel like this, then we apologize for the negative introduction. Please carry on as you were. For the rest of you, please read on as we try to clear up some of this demoralizing haze. By the way, U.S. stocks are up in the first half of the year…

Second Quarter Review

For the quarter, the S&P 500 fell 3.9%, following a very strong first quarter. The market posted its year-to-date highs early in the quarter and then experienced a fairly steep drop into early June. For the third year in a row, “sell in May and go away” was looking like an attractive trading tactic. June brought some relief, as European decision makers were able to make significant headway in dealing with the banking crisis there. Smaller cap stocks underperformed the S&P 500, as investors clamored for the perceived safety of larger names. European markets, to no one’s surprise, performed even worse. Emerging markets too fell in the wake of the global flight to quality and safety. Of the major equity indices, the Dow Jones showed the best performance for the quarter, further indicating the flight to quality manifest in the quarter.

Fixed income securities logged another solid quarter as the desire for safe returns rose in the face of fewer options for safety. Retail investors continue to pile into bond funds at a record pace. The data suggest that these investors are moving from cash into bonds, but there is some evidence that they may be selling some equity holdings to fund their bond purchases as well. U.S. Treasury bond yields have actually fallen well below the levels seen in the darkest days of the 2008-2009 crisis.

Here’s what the second quarter looked like by the numbers:

| Index | 2nd Qtr 2012 | Year to Date | Trailing 12 Months |

|---|---|---|---|

| Dow Jones Industrial Average | -1.8% | 6.9% | 6.8% |

| S&P 500 | -2.7% | 9.4% | 5.3% |

| NASDAQ | -5.1% | 12.7% | 5.8% |

| Russell 2000 | -3.5% | 8.5% | -2.1% |

| MSCI EAFE | -8.1% | 2.6% | -10.5% |

| MSCI EAFE Small Cap | -9.1% | 5.6% | -13.9% |

| MSCI Emerging Markets | -8.4% | 4.2% | -15.7% |

| Barclays Aggregate Bond | 2.0% | 2.2% | 6.9% |

| Barclays Municipal Bond | 2.0% | 3.2% | 9.7% |

| Dow Jones Commodities | -5.1% | -4.9% | -14.9% |

A Quick Look Behind the Curtain

Hello there. Mike Goodson here. I wanted to step away from the anonymous comfort of “we” to write you a few words in first person. For over four years now, I have been penning the quarterly letter for Wolf Group Capital Advisors. I actually wrote the first before I joined the company. You may want to speak with Bob about this sometime if you care for the details.

Over the course of my nearly-30-year investment career, I have written hundreds and read thousands of weekly, monthly and quarterly update reports. To be brutally honest, most of them are relevant for only a moment in time, surprisingly similar in tone and content, and regularly less than inspiring. They will often cover the basics – what has happened, why it happened and what might happen in the future. As a user of these reports, I would read them religiously, on the chance that one of them may contain an original thought or nugget of insight that would help my portfolios beat the market. I felt a lot like mining precious metals; I had to dig through a lot of dirt to find the good stuff.

As a producer of these quarterly reports here at The Wolf Group, I felt that I had two ways to go: 1) the traditional who/what/why approach or 2) something different. By October of 2008, it became obvious that our approach would be something different. The “Wizard of Oz” essay, written that month, cemented my style. In this piece, I drew analogies between the turbulent times we were facing in the capital markets at that time to the “Wizard of Oz” movie. The feedback was very supportive and I have tried to employ this style ever since, whether it involves basketball players, martyred saints or Einstein’s theories. The purpose is not only to update the reader on our views about the markets, but to entertain a bit and maybe even persuade the reader to think about something never before considered.

At this point, the structure of our quarterly reports should be very clear. The first and last parts are the more “traditional” elements of update reports. The middle part represents the “theme” sector where we try to get a bit creative and maybe have some fun. I suspect that some readers skip the middle part. Perhaps others only read the middle part. Regardless, this is how we do it, and we think it represents another unique offering from Wolf Group Capital Advisors.

This time around, however, we are trying something a bit different from our typically “different” approach. The middle part of this report will look and feel much more like a “traditional” quarterly update. In it, we will address many of the macro issues confronting the markets without any of the thematic trappings which we usually feature.

The Top-Down Approach

As part of our responsibility as wealth advisors, we need to understand what is happening in the world. We constantly monitor all important macro factors that might affect the capital markets. Some professional investors (the “top-down” ones) will craft portfolios exclusively based on their views of the big picture. For many, this approach has an attractive, intuitive appeal, given how much media coverage, political commentary and academic research appears to be focused on these issues.

The macro-approach investors right now are no doubt dealing with several important factors including China, Europe, Energy Prices, U.S. Housing and so forth. In an attempt to demonstrate our understanding of these issues, we will try our best to describe what is happening now and what might develop in the future.

China. The world’s second-largest economy is slowing. The big uncertainty here is whether the economy will slow from its historical 8-9% pace to something like 6-7%, or will it experience a “hard landing” and fall to something as low as 3-4%. The July 2, 2012 edition of Barron’s featured a cover story detailing all of China’s troubles – housing bubble, bad demographics, state-controlled banking sector, low consumer participation in the economy, and so forth. It was a compelling story, but we can produce other compelling research indicating a “soft-landing” is the most likely scenario due in part to the Chinese central bank’s willingness to ease monetary policy. Long-term, everyone seems to agree that China’s rising middle class is likely to benefit all industries that cater to this large and growing segment of consumers. So like many macro issues, it comes down one question: “Hard or soft landing?” Will China’s hard landing cause a global recession? Will avoiding a “hard landing” lead to higher than current global economic growth? These kinds of big questions we usually feel unqualified to answer. What does Mr. Market think about all this?

The chart below shows the price pattern of a Chinese equity market exchange-traded fund (ETF). From this chart one could argue that the time to become negative on China (from an equity investor point of view) was back in late 2010. We don’t recall any cover stories back then about China’s troubles. The stock market has fallen over 30% since then. We wonder how much of the “bad news” everyone is talking about now is already discounted by the Chinese stock market (and probably by other markets as well).

Europe. Europe is now in recession. Everyone knows this. Despite the current contraction of economic growth, almost no one expects the economy to sink into 2008- 2009 crisis levels. That is to say, it may be bad now, but is unlikely to get as bad as it has been. Recessions always end. Equity bull markets generally begin in the middle of recessions. Many of the stock fund managers we follow are growing more positive about European securities day by day. The equity markets over there are actually trading at large discounts to historical valuation levels. Yet, uncertainties abound. What will happen to Greece? Morgan Stanley published a piece a while back suggesting a 75% chance that Greece will exit the Eurozone. If the fallout from this is widespread, they think policy makers will have to act dramatically (create a euro-bond market, move toward a fiscal and banking union, etc.), and this will actually lead to higher-than-expected long-term economic growth. If the fallout is limited, the impact will be neutral to the economy, in their view. So what will happen, and what will the impact on the market be? Hard to tell. We would point out that nations may default, but unlike companies, are never liquidated. Recall Iceland’s recent bank failure. According to the experts, Iceland has recovered nicely from this crisis and is on the path to recovery. Greece may default and may exit the Euro, but it will not disappear.

What does Mr. Market think about Europe? The time to get negative on Europe was last May, given that the markets are down about 23% since then. We are not experts on Europe, but given the widespread pessimism we see now, it’s likely we are closer to a bottom than a top in Europe.

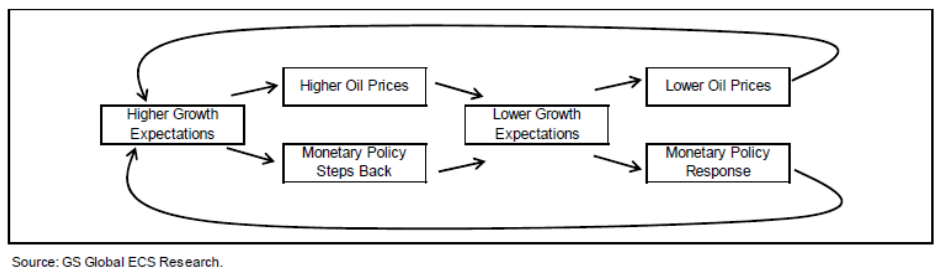

Energy Prices. Is there a commodity more linked to politics, policy and conspiracy theory than crude oil? When gasoline prices move dramatically in the U.S., politicians emerge quickly to take credit or lay blame. Rising oil prices are often met with a concomitant rise in the rhetoric about the need for alternative energy sources. Some serious commentators consider oil producers as some kind of evil cartel, whose sole purpose is to artificially inflate prices to punish consumers. The reality is probably that oil prices are impacted by the forces of supply and demand as well as overall global economic activity. In a recent report, Goldman Sachs provided a clear-eyed and unique take on how oil prices have impacted the economy over the last few years. They suggest that rising growth expectations will lead to higher oil prices and central banks moving away from an easy money policy. These two factors will have a dampening effect on the economy, which then leads to lower growth expectations. This in turn leads to lower oil prices and a resumption of monetary easing. This leads to higher expected growth and the mini-cycle repeats.

In our view, this would help explain, in part, the “stop and go” action the U.S. economy has displayed over the last few years. What we do know is that oil prices affect gasoline prices, and this can have an economic and psychological impact on the U.S. consumer. Thus, the recent trend for lower gasoline prices should have a positive impact on the U.S. consumer, which could help economic growth in the second half of the year.

What does Mr. Market think about oil prices? They are well below peak levels of 2008 and have basically followed the pattern suggested by Goldman’s report. The annual peaks in oil prices have occurred just before the economic slowdowns recorded each year. A curious correlation!

U.S. Housing. Everyone knows that housing in the United States was a large contributor of economic growth from 2004 to 2008. The fact that this bubble burst with devastating consequences is also well known. Where does housing stand now? To start with, the current economic expansion (yes, believe it or not the U.S. economy has been out of recession since June 2009) has occurred without any help from the housing industry. The average person probably has not noticed that most recoveries are fueled by something other than what helped that last one, be it bank loans, business spending, job growth or whatnot. Thus, one perspective to consider is that the economy has grown despite the worst housing market since the Great Depression. In addition, this economy has faced the headwind of household deleveraging, something somewhat related to housing. Maybe 2% GDP growth should be celebrated given these factors?

A recent report from Morgan Stanley suggests that the distressed segment of the housing market is bottoming. They noted that they were “cautiously optimistic” about the prospects for housing, but they cautioned that a “prolonged bottom” is also a likely scenario. They opined that significant job growth and reforms in mortgage practices were needed before the housing market could recover in a meaningful way.

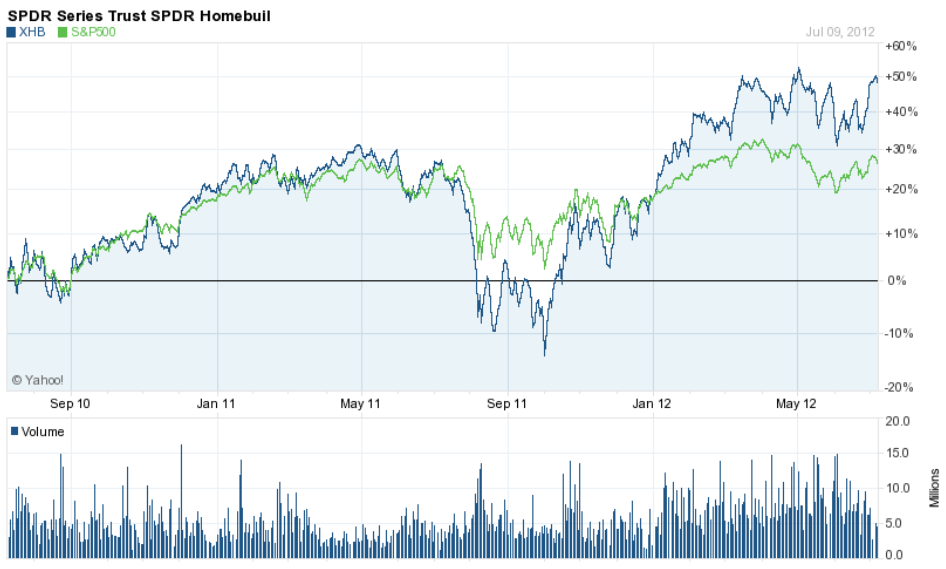

What does Mr. Market think? There may not be a really good stock market proxy for the housing market, but one could argue that the fortunes of the home building companies are correlated with the overall housing market. Below is a chart of a home builder ETF. It shows home building stocks up 50% over the last two years versus the S&P 500’s +27%. A longer chart would show that the home builders bottomed out in March of 2009. The housing industry may still be in a funk, but shareholders of the home builders have been richly rewarded by buying them in the midst of this funk.

So, what can we conclude from all of this? 1) A China slowdown will either blow up the world’s economy or not. 2) Greece leaving the Eurozone may increase regional growth or not. 3) Oil prices may actually drive U.S. economic growth, but it’s hard to predict where oil prices will go. 4) The U.S. housing industry may be bottoming out, but it might be too late to invest in it via the equity market.

The real trick now would be trying to create (or modify) a portfolio based on these “conclusions.” In our view, this exercise underscores the difficulty in investing from a “top-down” approach. Many of the biggest macro questions facing us today may be impossible to answer with the clarity that we would like. Making a bet one way or another on any of these issues seems much more like speculation than investing, in our opinion. The other huge challenge to investing this way is trying to figure out exactly how much of the big picture factors are already discounted by the market. That is to what extent are future scenarios already reflected in asset prices?

The Bottom-Up Approach

Our approach to investing is decidedly bottom-up. That is we focus on individual companies rather than on the overall market. In fact, in our internal discussions about important investment issues, whenever someone begins to talk about the “market,” inevitably someone will quip in counterpoint, “Good thing we don’t invest in the market…” We spend the bulk of our investment research effort on trying to assess the value of companies and seeking out those most undervalued by the market. We understand that many people believe the markets are efficient, but our personal experience (supported by tons of academic and practitioner research) suggests that lots of inefficiencies exist in the prices of equities. Skillful, dedicated and persistent research can capitalize on these pockets of mispricing. This is what we try to do for our clients who hold individual stocks in their portfolios, and also what the professional portfolio managers who take care of our mutual fund clients do.

Focus on the Company

We approach investing in equities much like we were buying a house. We want to know everything about it – its history, what changes it has been through over the years, former owners, the neighborhood, trends in the neighborhood and then last and most importantly, the price. No one would buy a house just because someone told them it might be a good thing to do. No one would buy house because it was blue or had a fancy front porch. Finally, no one would buy a house without some understanding of its value. We find it baffling that the same people who can buy a house by applying all the necessary and important research will buy a stock with total disregard to any of these principles. People buy stocks every day based on a comment heard on television, a tip from a relative, a fancy story weaved by a broker or a random article in the newspaper

We spend as much of our time trying to understand the value of a stock as we do the story. We wanted to share with you a few of the names we like right now and how we look at them.

The data included in this letter was obtained from sources Wolf Group Capital Advisors believes to be reliable, but do not guarantee the accuracy, and such information may be incomplete or condensed. This is for informational purposes only, and is not intended to be an offer, solicitation, or recommendation with respect to the purchase or sale of any security, or a recommendation of the services offered by any money management organization. Investing in securities is speculative, carries a high degree of risk, and positive performance cannot be guaranteed.

OM Group (OMG)

OM Group is a small, but diversified specialty chemicals and materials company. For years, the bulk of its product lines used the metal cobalt as a key component. As such, its earnings were quite volatile, rising or falling with the price of cobalt. Recently, it has been acquiring additional lines of business in an effort to reduce earnings volatility and its dependence on cobalt. Over time, we think that the result of these diversification efforts should lead to a higher valuation on the shares. Not too long ago the company earned well over $5 per share. At that time, the market afforded it a modest price-toearnings (P/E) ratio of 9.5x. We expect the company to earn more than $5 per share again, and given that these earnings will be less reliant on cobalt, we could see a valuation of more than 10 times on the shares.

Seagate (STX)

Seagate is roughly one half of the global duopoly in hard disk drives. Disk drives are the main way electronic data is stored everywhere around the world. It is a challenging technology, trying to cram more data into a fixed amount of space. The industry is also being threatened by solid state memory devices which have no moving parts. But, until every bit of digital media is available on every digital piece of hardware in the world, the need for data storage will increase. We think Seagate will benefit from this growth. In fact, Wall Street analysts think that the company can grow earnings in excess of 30% over the next five years. What about valuation? Right now the shares are trading at 3.7x this year’s earnings. The shares also offer a dividend yield of 4%. Compare these numbers with the S&P 500 – P/E of 12.8x, yield of 2% and earnings growth of maybe 10%. If these estimates for Seagate prove correct, the stock is trading at less than a third of the market’s valuation, with triple the potential growth and double the dividend yield. This is why we like it.

Avon Products (AVP)

Avon makes and markets beauty-related and other products via independent direct sales representatives throughout the world. The term “Avon Lady” conjures up the oldfashioned notion of a middle-aged woman sitting on your grandmother’s couch selling her perfume and lipstick. Today the company is embroiled in bribery scandals, turmoil at the CEO position, disgruntled sales reps, shareholder lawsuits and an ill-advised rebuff of a takeover bid. This is not your grandmother’s Avon! So, what’s to like? The company offers one of the best platforms for women in the emerging markets to become entrepreneurs. The company provides low-cost products that sell well in these markets and great support to their sales reps. To an important extent, growth in the emerging market economies will be very good for Avon. The market understands all of the company’s current ills and is awarding it a very low valuation, only 13x next year’s earnings. Typically, a company like this should trade at 17-18x. The shares also offer an amazing dividend yield of 5.6%. Some people think this could be cut, but even at half of that, the total potential return looks very attractive. Consider too, that not too long ago one smart company thought Avon was inexpensive enough to offer to buy the entire company. We think that another potential suitor might materialize sometime in the future. It is a stock not without risk, but we think the potential rewards outweigh the risks. This is why we like it.

These are just three of the stocks featured on our Buy List. If you happen not to see these names in your portfolio, no need to worry. We have 80 other names on our Buy List which we like just as much. We use the stocks on our Buy List to create individual equity portfolios for those clients for whom they are appropriate. This is our bottom-up approach.

The Outlook

We continue to think we are in a bull market for stocks and close to a peak in bond prices. Cash continues to be the most dangerous thing to hold, in our view.

We recently read a report by John Calamos, the CEO of Calamos Investments, in which he describes the three legs of a bull market. Because we continue to think that we are in a bull market (it started back in March 2009), we found Mr. Calamos’ views on the matter intriguing. His first leg was economic growth. Given the less-than-perfect correlation we see between the economy and the stock markets, we were skeptical at first about this leg. His conclusion was that a growing global economy, even if it slows a bit, would be supportive of the bull market. For us, we think that earnings would be a better leg to stand on, but earnings are clearly driven in part by economic growth. Either way, the first leg is secure. Absent a global recession, stocks should be supported by economic growth.

His second leg was liquidity. This is manifest by the large amount of “money on the sidelines” (not invested) and an even bigger amount invested in low-yield bonds. We have not yet seen investors sell bonds and buy stocks, or use large amounts of cash to buy stocks. His point (and we agree) is that all this cash and all these low-yield bonds represent highly dry kindle that could easily spark a major stock market rally, if and when investors regain confidence in equity investing. We think this is likely to happen only after stock prices go up a lot. We think it would make more sense to own stocks now before that happens.

The third leg was equity valuation. According to his company’s research, stocks are undervalued globally, using any number of metrics – book value, earnings, cash flow and so forth. This means that stocks are on sale, and who doesn’t like a sale? Recent research by Goldman Sachs quantified this undervaluation for the U.S. stock market. They suggested under the current state of affairs, the S&P 500 (a good proxy for the “market” in our view) should be trading at 17 times earnings. Now it’s trading at about 12.8 times. We note that valuation alone is rarely a good reason to buy stocks, but it is an indication of how “popular” they are. They seem out of favor now, and historically, that has always been a good time to buy.

As usual, we don’t know for sure what’s going to happen over the next 6 months or 12 months. We do know that many stocks are trading at attractive discounts to their fair value. We also know that equities have always afforded the best returns of any asset class over time. We are comfortable in letting all the “experts” debate about the fate of the world, while we quietly seek value where we can.

Sincerely,

Wolf Group Capital Advisors