On December 22, President Trump signed into law the most sweeping changes to the tax code in over 30 years. No one is left untouched. Individuals, corporations, sole proprietors, partnerships, S corporations, and multinational businesses are all affected.

As the individual income tax debate raged in Congress, rates were uncertain, and all sorts of deductions and credits were on the chopping block.

- Would individuals be able to deduct medical expenses?

- Would Head of Household filing status go away?

- Would individuals be able to deduct state income taxes, property taxes, and sales taxes? If so, would there be limits?

- Would the Alternative Minimum Tax be eliminated?

- If an individual sold a house, how long would he or she have to have owned it and lived in it in order to exclude part of the gain from tax?

These questions were being debated until the last minute, and the media reported each oscillation.

As a result, many individual taxpayers have questions regarding which provisions were only discussed and which actually made it into the final legislation.

To provide clarity on this matter, the following paragraphs examine a few of the most common tax areas of interest to individual taxpayers and explain the outcomes under the new legislation. Due to the length and breadth of the new legislation, we focus here only on certain highlights related to individual taxation, and we anticipate issuing future articles related to the treatment of sole proprietorships, pass-through entities, and other entities under the new law.

It is important to note that most of the changes described below begin with the 2018 tax year and sunset after December 31, 2025. Future legislation will be necessary to extend these tax provisions; otherwise, they will revert to the rules in effect before the tax reform was passed.

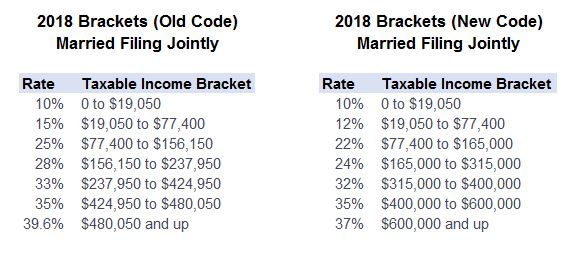

What happened with individual income tax rates?

The new tax law has kept the 7-tax bracket structure, generally lowered tax rates, and increased the threshold for each tax bracket. For example, here are the Married Filing Jointly tax tables for 2018 before and after the new tax law passed.

Were any filing statuses changed or eliminated?

The new law does not change any filing statuses. The statuses remain:

- Single

- Married Filing Jointly

- Married Filing Separately

- Head of Household

- Qualifying Widow(er) with Dependent Child

Can a personal exemption of $4,050 still be claimed for each person (taxpayer, spouse, and dependents)?

For 2017, a personal exemption of $4,050 may be claimed as a deduction for the taxpayer, spouse, and each dependent, although this deduction is phased-out beginning at an adjusted gross income (AGI) level of $313,800 (Married Filing Jointly) and $261,500 (Single).

For 2018 and future years, the new law completely eliminates the deduction for personal exemptions. Since the personal exemption is repealed, the phase-out is also repealed.

What were the final changes to the standard deduction?

An individual is allowed to deduct the greater of the “standard deduction” or itemized deductions. For 2017, the standard deduction is $12,700 for Married Filing Jointly and $6,350 for Single.

For 2018, the law substantially increases the standard deduction to $24,000 for Married Filing Jointly and $12,000 for Single filers.

Many itemized deductions were heavily debated. What was the final outcome?

Medical Expenses

Although lawmakers considered eliminating the itemized deduction for medical and dental expenses, in the end, they allowed a greater deduction (temporarily) for these expenses. Through the 2016 tax year, the deduction was allowed only for expenses that exceeded 10% of the individual’s AGI.

Under the new law, the AGI threshold is reduced to 7.5% for 2017 and 2018 but reverts to 10% beginning with 2019.

State and Local Income and Property Taxes

Lawmakers heavily debated eliminating or limiting the deductions for state and local taxes. For 2017, individuals may continue to claim itemized deductions for state and local income taxes and state, local, and foreign property taxes on their 2017 returns.

Beginning in 2018, only up to $10,000 in combined state and local income taxes and property taxes will be deductible as an itemized deduction. (The limitation is $5,000 for a married taxpayer filing a separate return). Foreign property taxes will no longer be deductible. (NOTE: the new limitations do not apply to property taxes paid on a rental property or deductible by a trade or business.)

Also, the new law does not allow an individual to claim an itemized deduction in 2017 on a pre-payment (in 2017) of 2018 state and local income taxes.

Home Mortgage Interest Deduction

Although lawmakers considered significantly reducing the deduction for home mortgage interest, the new law continues to allow individuals to claim itemized deductions for home mortgage interest for a principal residence and one other residence. In 2017, home mortgage interest may be deductible on up to $1 million of “acquisition indebtedness”; that is, for acquiring, constructing, or substantially improving a residence. Individuals may also claim interest on up to $100,000 in home equity indebtedness.

The new law reduces the mortgage interest deduction to interest on up to $750,000 of acquisition indebtedness for debt incurred after December 15, 2017. The $1 million limitation is still in place for debt incurred prior to December 15.

Beginning in 2018, the new law eliminates the interest deduction for interest on home equity debt. Note that interest on home equity debt is not grandfathered, and therefore this type of interest will no longer be deductible.

Charitable Contributions

Generally, for 2017, a taxpayer is allowed to deduct cash contributions to qualified U.S. charities, but the deduction cannot exceed 50% of AGI. Beginning in 2018, the new law increases the AGI limitation from 50% to 60%.

Personal Casualty & Theft Losses

For tax year 2017, taxpayers may generally claim an itemized deduction for personal casualty losses that arose from fire, storm, other casualty, or theft, to the extent that these losses exceed 10% of the taxpayer’s AGI.

The new law provides that beginning in 2018, the deduction may only apply to losses that are incurred as a result of federally declared disasters.

Miscellaneous Itemized Deductions

Through tax year 2017, an individual may deduct certain expenses as “miscellaneous itemized deductions” to the extent they exceed 2% of the taxpayer’s AGI. These expenses generally fall under the following categories: unreimbursed employee business expenses; investment management fees and other expenses incurred to manage or maintain property held for producing income; and tax preparation fees.

For 2018 and future tax years, the new tax law eliminates the deduction for all 2% miscellaneous itemized deductions.

Was the Alternative Minimum Tax eliminated?

The Alternative Minimum Tax (AMT) was on the chopping block during tax reform debates, but ultimately, it was adjusted rather than eliminated.

In order to determine whether a taxpayer is subject to the AMT, one must calculate the tax liability for regular income tax purposes and then recalculate it for AMT purposes. The taxpayer pays the greater of the regular or AMT liability.

In the calculation of AMT, individuals are allowed an exemption amount, assuming that their income does not exceed certain thresholds. If income exceed those thresholds, the exemption is phased out. The new law increases the exemption amounts from $84,500 for joint filers and $54,300 for single filers (in 2017) to $109,400 and $70,300, respectively, for tax years beginning in 2018. In addition, the exemption phases out at much higher income levels, beginning in 2018.

What changed for child tax credits? Will more people be able to claim them?

For 2017, taxpayers may be eligible for a $1,000 tax credit for each qualifying child under the age of 17. Child tax credits are phased out for those taxpayers with an AGI over $75,000 for single filers and $110,000 for joint filers.

Under the new law, for tax years beginning in 2018, the child tax credit is increased to $2,000, and many more taxpayers may be able to take advantage of the credit since the AGI thresholds at which the credit begins to phase out are increased to $200,000 for single taxpayers and $400,000 for joint filers.

Also, the new law provides that a $500 credit is available for dependents other than qualifying children.

Can I still deduct my moving expenses for a job-related move?

Generally, prior to 2018, an individual who had a work-related move was potentially eligible to claim a deduction for moving expenses. However, for tax years beginning in 2018, the new law eliminates the moving expense deduction, except for certain active duty members of the Armed Forces.

Did the rules change for excluding the gain on the sale of my home (primary residence)?

Both the House and Senate bills contained proposals that would have changed the holding period required to obtain the principal residence exclusion, but these proposals were eliminated at the last moment in the Conference Committee and so were not enacted.

Who will pay the tax on alimony payments?

Currently, in most cases, the payor of alimony is allowed a deduction (not subject to the itemized deduction limitations), and it is the payee who must include alimony payments in taxable income.

For divorce agreements executed after December 31, 2018, the new law generally eliminates both the ability of the payor to claim a deduction for alimony and also the requirement that the payee include the alimony in taxable income.

What happened to the tax rates for dependent children with investment income?

For tax year 2017, a child is taxed on his or her unearned income (e.g., investment income) at the higher of the parents’ tax rates or the child’s rates.

Beginning with tax year 2018, the new law simplifies the way a child’s net unearned income is taxed. Rather than applying the parents’ or child’s rates, the law calls for trust and estate tax rates to be applied. Trust and estate tax rates are steeply progressive; for example, for 2017 the highest tax bracket of 39.6% is reached at a taxable income level of only $12,500.

What happened with capital gains rates and qualified dividends?

The new law will not change the way capital gains and qualified dividends are taxed. Net capital gains and qualified dividends will continue to be subject to tax at a maximum rate of 15% or 20%, depending on a taxpayer’s income level. The income level that shifts a taxpayer into the 20% capital gains bracket will be the same as in 2017—$479,000 for married taxpayers filing jointly and $425,800 for single filers. The new law also leaves in place the current 3.8% Net Investment Income Tax implemented to help fund the Affordable Care Act.

***

The new law was passed quickly. Will there be changes?

The new tax legislation was completed and passed in a matter of a few months. Lawmakers, businesses, individuals, and tax professionals have already identified a number of areas of ambiguity, typos, and other issues that need to be addressed so that taxpayers have a clear understanding of how to comply with the law and calculate their taxes.

Generally, such issues would be addressed in a technical corrections bill. The challenge, however, is any technical amendments would require bipartisan support to pass, whereas the initial law only required a simple majority (more than 50%) to enact.