Some people feel the need to climb a mountain to seek the wisdom of some sage ascetic. Others find comfort in conforming to popular trends. Investment styles can also vary greatly. Some feel comfortable owning “the market” using exchange-traded funds (ETFs) as the bulk of their portfolio. Others avoid investing altogether and keep their wealth in the false security of cash. Others try to generate profits by capturing the short-term movements in prices. Some will employ highly sophisticated computer models to tell them what and when to buy/sell. The clever thing about the investment process is that there is no one “right” way to invest. The markets work exactly because many smart (and perhaps not-so-smart) investors are using their own particular investment strategy to try to make money, preserve capital or plan for long-term goals such as retirement. In a very real sense, the price of any given investment asset is set by the collective decisions of these thousands of investors. Over the last three months, the net result of all these investor decisions was higher stock prices. With prices now near all-time highs, many are wondering what now to do. Some fear that the market has come too far, too fast. Others worry about another global financial crisis, or some other “black swan.” In times like these it may be good to ask “What would Warren do?”

First Quarter Review For the quarter, stock market returns were very strong. It’s as if all the “stuff” that created so much angst in the fourth quarter (fiscal cliff, higher taxes, sequestration, debt level negotiations, etc.) simply vanished, leaving the market with only one way to move — higher. The underlying fundamentals have been strong for many quarters, but they often would be obscured by some perceived big crisis just ahead. One new factor seen this quarter was retail investor buying of U.S. equities. The funds flow data suggests that retail investors put $ 75 billion into stocks and stock funds in the first three months of 2013. This was in stark contrast to the $150 billion they pulled out of stocks in 2012.

As one might expect, fixed income securities provided only modest returns, but continued to show positive returns as investors are convinced that higher interest rates are unlikely in the face of the Fed’s pledge to keep them low. The latest plan for quantitative easing has only reinforced this conclusion. During the quarter, retail investors continued to add to their bond investments, albeit at a slower pace than before. It appears that the massive stockpile of cash is slowly being deployed into the capital markets. The emerging markets are still lagging the developed ones, and weak commodity prices continued in the quarter.

Here’s what the first quarter looked like by the numbers:

| Index | 1st Qtr 2013 | Year to Date | Trailing 12 Months |

|---|---|---|---|

| Dow Jones Industrial Average | 11.9% | 11.9% | 13.4% |

| S&P 500 | 10.6% | 10.6% | 14.0% |

| NASDAQ | 1.4% | 1.4% | 5.7% |

| Russell 2000 | 12.4% | 12.4% | 16.3% |

| MSCI EAFE | 5.1% | 5.1% | 11.3% |

| MSCI EAFE Small Cap | 8.0% | 8.0% | 13.4% |

| MSCI Emerging Markets | -1.9% | -1.9% | -0.6% |

| Barclays Aggregate Bond | 0.1% | 0.1% | 3.8%/td> |

| Barclays Municipal Bond | 0.3% | 0.3% | 5.3% |

| Dow Jones Commodities | -1.8% | -1.8% | -4.0% |

Who’s the Best Investor Ever?

Perhaps this question is something only investment nerds really care about. It might come off a bit like high school kids debating who the best baseball pitcher is, or which pop singer is the best. Yet, somebody (some investment nerd probably) has done some research that can help us answer this question. Rediff.com compiled a list of the 26 wealthiest people of all time. #1 on this list is Mansa Musa I of Mali. His kingdom, which flourished during the 14th Century, comprised a wide stretch of land from the west coast of Africa into the middle of the continent as far as modern day Chad. He is famous for making Mali an economic global power, and an intellectual center with a world-class military power. Along the way, he amassed a fortune worth (in today’s dollars) something close to $400 billion.

The rest of the list is populated with the expected assortment of European kings, third world despots and 19th Century U.S. industrialists. Appearing on this list at #25, and the only person on the list who we would consider a traditional “investor,” is Warren Buffett. Mr. Buffett’s reputation and fame is truly legendary among professional investors. His life and success as an investor has been chronicled countless times, and a comprehensive review of his story is well beyond the scope of this report. Yet, we always find it rewarding and instructional to share with our clients his insights and opinions about the investment process.

The Sage of Omaha

We assume most people know the basics of the Warren Buffett story. He was born in Omaha and lives there still. He bought his first stock in 1942 and now has a personal net worth of over $50 billion. He drives an old, beat-up car. He is a world-class bridge player. He plans to give most of fortune to charity when he dies. Most important to the theme of this report is his adherence to the discipline of value investing.

As a student at Columbia University under the father of value investing, Benjamin Graham, Buffett embraced this philosophy early on. He was enamored by the notion that one could buy a portion of company (a stock) at a price below what it was really worth. As his wealth grew, he was able to buy larger and larger stakes in companies. His company currently owns massive positions in many blue chip names – $8 billion of American Express (AXP), $14 billion of Coca Cola (KO), $13 billion of IBM (IBM), etc. Eventually, he amassed sufficient wealth to actually buy entire companies, not just a piece of them. Famous examples of these are See’s Candies, GEICO, Burlington Northern, and his most recent large acquisition, H. J. Heinz. Most of these companies are contained within the structure of his publicly-traded holding company, Berkshire Hathaway (BRKB).

Apart from his wealth, he is famous for keeping his head when the rest of the world seems to be losing theirs. As a large shareholder of the investment bank, Salomon Brothers, he actually became chairman of the firm in the early 1991 following a management scandal. During the global financial crisis of 2008-2009, he was very active providing needed capital to General Electric (GE), Goldman Sachs (GS), and Swiss Re. Like most of his investments, these ventures have proved to be highly profitable to Mr. Buffett, his company and its shareholders.

Revelations from the Midwest

Unlike the stereotypical guru, Mr. Buffett is not hid away atop some remote mountaintop. He can be found in the middle of the United States working in his modest office in Omaha, Nebraska. And, unlike the stereotypical secretive billionaire (think Howard Hughes), he is quite accessible. He speaks to the press often, he accepts the spotlight (but not seem to crave it), and as the largest shareholder of a famous public company, pens an annual report letter than is widely read by investors and regular folk alike.

As usual, this year’s letter was outstanding. In it, he was in turn, funny, insightful, humble, instructional and very detailed in how he thinks, runs his business and approaches the discipline of investing. In our view, the entire letter is a “must read” for anyone with any interest in investing, how to run a business or simply how a very successful businessperson views the world. Here is a link to the letter: http://www.berkshirehathaway.com/letters/2012ltr.pdf

Given our infatuation with Mr. Buffett, we thought we would share a few gems from his most recent letter that we think well support some of the fundamental investment principles we use to help our clients reach their financial and life goals.

Timing the Market. We have always preached about the perils of market timing. We don’t try to time the market, and most studies we have seen suggest that no one can consistently make money investing this way. As soon as someone sells stocks with the intention of buying them back at a lower price, they have created a stressful situation which is difficult to resolve. If prices move higher, what should one do? If prices go lower, how low must they go before one will want to buy? Most people find it very stressful to buy stocks when prices are declining. Mr. Buffett agrees, but actually throws another concept into the mix to make the case against market timing.

After pointing out that “American business will do fine over time,” he offers this very valuable (in our view) advice, “Since the basic game [of investing] is so favorable, Charlie [his long-timer business partner Charles Munger] and I believe it’s a terrible mistake to try to dance in and out of it [the market] based upon the turn of tarot cards, the predictions of “experts,” [he uses quotation market around the word, just like we often do] or the ebb and flow of business activity. The risks of being out of the game are huge compared to risks of being in it.”

We concur. Investors will always do better by sticking to a well-crafted investment plan than trying to invest based on current trends, fads, “expert” views or by timing the market.

Uncertainty. We sometimes speak with people who are uncomfortable investing in “times of uncertainty.” Try as we may, we find it hard to explain that the best time to invest is when one feels the worst and uncertainty seems to be very high. Intuitively, it’s easy to think that it’s smart to invest in the markets in good times. Empirically, the opposite is true – the times of greatest anxiety and uncertainty are the best times to buy stocks.

In his letter, Mr. Buffett adroitly addresses this notion. “There was a lot of hand-wringing last year among CEOs who cried “uncertainty” when faced with capital-allocation decisions (despite many of their businesses having enjoyed record levels of both earnings and cash). At Berkshire, we didn’t share their fears, instead, spending a record $9.8 billion on plant and equipment in 2012, about 88% of it in the United States… Charlie and I love investing large sums in worthwhile projects, whatever the pundits are saying… Opportunities abound in America. A thought for my fellow CEOs: Of course, the immediate future is uncertain; America has faced the unknown since 1776. It’s just sometimes people focus on the myriad of uncertainties that always exist while at other times they ignore them.”

We often say that at any point of time there are negatives and positives about the market. Sentiment is simply a function of where people are placing emphasis. It is very rare to experience a time when there appears to be no uncertainty. Those times, like the late 1990s, tend to define secular market peaks.

Intrinsic Value. This principle defines the key element of value investing. In our view, “intrinsic value” means the value of something (in finance, usually a company or a stock) determined through fundamental analysis without reference to its market value. In its most elemental form, value investing is simply buying things which are trading in the marketplace at a discount to their fundamental, fair, or intrinsic value. Although this may sound simple and easy, determining intrinsic value requires as much art as science, as does actually having the conviction to act on one’s analysis.

Mr. Buffett’s investment style reflects his penchant for value investing. He tends to look at companies with a consistent track record, low debt, rising profit margins, etc., and would like to buy them at a discount of 25% or more from his estimate of intrinsic value. Again, this may sound like simply formula, but as in most things, proper execution of the formula makes all the difference.

Mr. Buffett’s investment in Goldman Sachs (GS) provides an excellent example of how he uses value investing principles to his and his shareholders’ advantage. In September of 2008, directly after the implosion of Lehman Brothers and the government bail-out of American International Group (AIG), investment banks such as Goldman Sachs were looking for help to survive. Many of them became bank-holding companies in order to qualify for some government help. Others, like Goldman, also turned to Mr. Buffett for help. He bought $5 billion worth of preferred shares that paid a 10% dividend, or $500 million per year. He was also awarded (at no cost to him) warrants that would allow him to buy $5 billion of Goldman common stock at $115. Goldman welcomed his investment because it gave the company much needed capital at a crucial time. Some may have viewed his investment at this time as reckless or even foolish, but at that perilous time he understood the intrinsic value of Goldman Sachs’ franchise and calculated that this investment would be profitable and helpful to both parties.

It was. Goldman survived and Mr. Buffett made a $1.7 billion profit on his investment, and last month he exercised the warrants making him the top shareholder of the company. He has announced that he plans to remain a long-term investor in the company. Goldman Sachs’ management has commented that they are very happy to have Mr. Buffett’s company as a long-term investor. Given his track record, this could be the beginning of a mutually beneficial relationship.

We consider ourselves value investors. We spend a great deal of our research effort looking at the fundamentals of companies. We use many of the same criteria Mr. Buffett employs when looking for new investments. We try to avoid investment fads and the popular trends that arise now and then. Although our size and success are dwarfed by Mr. Buffett, we find great comfort knowing that in some small way we are at least on the same team.

What Would Warren Do Now?

In a way, this is a trick question. We think Mr. Buffett does today which he does every day – in all seasons and at all points of the economic and market cycle. Value investing releases one from the day-to-day macro concerns which consume so much time and effort of most people who invest in some other way. We suspect that right now he is analyzing companies, looking for great businesses at a fair price, just like he always does.

In the worst of times in 2008, he was buying when almost everyone else wanted to sell. Even after the market bottomed in 2009, he found good value in Burlington Northern. Even after the market had risen 100% from its 2009 lows, he found good value in Heinz. Because he does not focus on the economy or the market, he has great freedom to look at investments in a different light than many others. He looks at owning shares in a company just like owning a company. He wants to understand intimately what makes the company and its management tick. He wants to share in their success. We think many people look at owning a stock like owning a piece of paper or even a lottery ticket. We think that anyone willing to spend some time and effort understanding how Mr. Buffett invests would be well educated and well rewarded for their efforts.

The Outlook

During the quarter some of the big stock indices reached new highs. Whenever this happens, many people begin to wonder if the markets can go higher. The long-term answer to this question is “always.” The experience of investors over the last 13 years may make them wonder if this will be the case in the future. We think it will.

Mr. Buffett actually has something to say about this idea in his latest letter. “… I made my first stock purchase in the spring of 1942 when the U.S. was suffering major losses throughout the Pacific war zone. Each day’s headlines told of more setbacks. Even so, there was no talk about uncertainty; every American believed that we would prevail. The country’s success since that perilous time boggles the mind: On an inflationadjusted basis, GDP per capital more than quadrupled between 1941 and 2012. Throughout the period, every tomorrow has been uncertain. America’s destiny, however, has always been clear: ever-increasing abundance.”

We continue to think that fundamentals support our bullish view on stocks. We are less bullish on bonds, but we think that short-rates are unlikely to rise significantly as long as Central Banks around the world are easing. The key wildcard to our outlook is sentiment. Early in the year, we heard a lot of talk about the “Great Rotation” where individual investors would begin selling their bonds and buying stocks. The implications for stocks are very positive.

We think the jury is still out on this. Retail investors have been buying stocks so far this year, but we wonder how they will react if the market corrects a bit (like it has each of the last four years). In the past, these corrections were interpreted by the “experts” and by retail investors, not as a temporary pause in the bull market or as a buying opportunity, but as the beginning of something new and really bad. Retail investors sold on weakness in each of these corrections. If we see retail investors finally buying on price weakness this year, we would be inclined to admit that a “Great Rotation” may be afoot.

We continue to think we are in a bull market in stocks. One could make a solid argument that the current bull market and economy recovery are just getting started. True, they both are about as old as “normal” recoveries/bull markets are, but there are enough differences to make us think we still have considerable upside to the economy and stock prices.

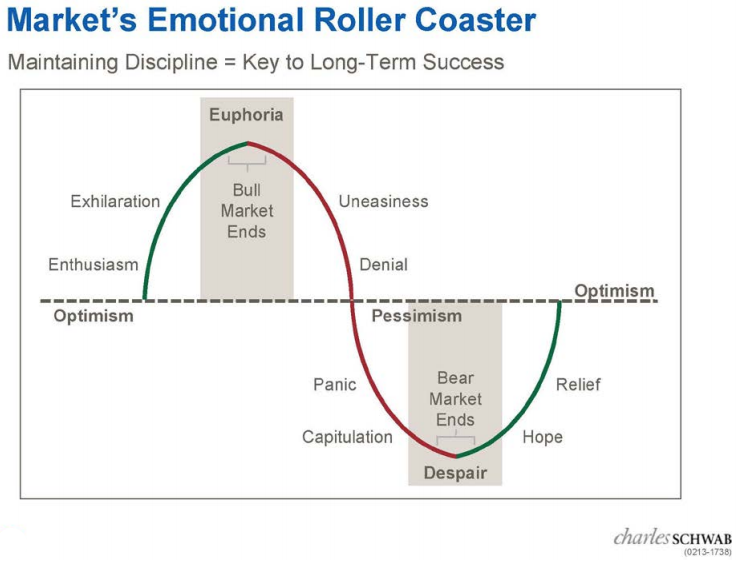

Liz Ann Sonders, the Chief Investment Strategist for Charles Schwab & Co., uses the following to depict how sentiment fluctuates in a typical bull/bear market cycle.

We all know that the last bull market ended in 2007. We also have all felt the uneasiness, denial, panic, capitulation and despair of the bear market which lasted until early 2009. From the bottom of the market, we can clearly mark the periods of hope and relief investors felt from then until now. Where do you think we are in this cycle?

Our view is that we may have just crossed the “Optimism” line and have before us the enthusiasm, exhilaration and euphoria that usually accompanies the second half of a bull market. Bull markets rarely end with this much negativity and worry out there.

Sincerely,

Wolf Group Capital Advisors