“Facts are stubborn things; and whatever may be our wishes, our inclinations, or the dictates of our passion, they cannot alter the state of facts and evidence.” – John Adams, the second President of the United States.

A recent Google search on the word “data” yielded 25.27 billion results in 0.29 seconds. Twenty-five billion is a big number. It is 3.5 times the number of people on Earth. Twenty- five billion seconds would be almost 800 years. In light years, it would represent two times the deepest view ever of the universe (thanks to the Hubble Space Telescope). Still, having an Internet search spit out 25 billion results in less than one-third of a second is something we all do many times (billions?) each day. The amount of data available on the Internet staggers the imagination. Most Internet users have the confidence that nearly any question can be answered quickly and accurately via a simple search. With just a few mouse clicks, we can find just about anything imaginable. Despite the unprecedented amount of data available to the modern person, many people still struggle to understand how the capital markets operate and why there are so many different opinions out there, if indeed, everyone is looking at the same data. In this edition, we will attempt to clear up some of the confusion…

Third Quarter Review

For the quarter, the data speak for themselves. Stock market returns were strong; the bull market that began in early 2009 marches on. The markets paused a bit when investors began to worry about the impact the U.S. Federal Reserve’s decision to “taper” (reduce monthly bond purchases) might have on the economy and capital markets. However, in the end, strong economic fundamentals and the Fed’s decision to maintain its aggressively easy monetary policy stance helped propel stock prices higher. Bonds continue to ping pong between the widelybelieved inevitability of higher interest rates and their status as a safe haven in times of uncertainty. The yield on the U.S. 10-year Treasury note breached 3% during the quarter before backing down as the threat of a U.S. government shutdown loomed. Weakness in the emerging markets hurt not only equity returns there, but also commodity prices generally.

Here is what the third quarter looked like by the numbers:

| Index | 3rd Qtr 2013 | Year to Date | Trailing 12 Months |

|---|---|---|---|

| Dow Jones Industrial Average | 2.1% | 17.6% | 15.6% |

| S&P 500 | 5.2% | 19.8% | 19.3% |

| NASDAQ | 10.8% | 24.9% | 21.0% |

| Russell 2000 | 10.2% | 27.7% | 30.1% |

| MSCI EAFE | 11.6% | 16.1% | 23.8% |

| MSCI EAFE Small Cap | 15.7% | 20.8% | 29.4% |

| MSCI Emerging Markets | 5.0% | -6.4% | -1.5% |

| Barclays Aggregate Bond | 0.6% | -1.9% | -1.7% |

| Barclays Municipal Bond | -0.2% | -2.9% | -2.2% |

| Dow Jones Commodities | 2.1% | -9.9% | -15.7% |

Looking for Mr. Data

The Internet provides us with a vast amount of information at our fingertips. Nearly instantaneous dissemination of this information leads to an odd mix of enlightenment and confusion. On any given day, we can learn in detail about some significant event in a faraway country and then run into a bogus story about a miracle cure or fake political scandal. In simpler times, we would receive our news via one of three national outlets and a local newspaper or two. Competition among the news providers created a certain level of quality, objectivity and tone that provided comfort to the consumer that the news they were receiving represented a proximate version of reality.

Nowadays, with countless choices for news and the ever-expanding number of bloggers, the information consumer faces a big challenge: how to separate the wheat from the chaff, the truth from the conjecture, and ultimately the facts from opinions. We feel that this process of sorting the useful from the dross is particularly important in matters related to the financial markets. On any given day, one can find literally hundreds of articles, broadcast segments or blogs offering supposedly valuable investment advice. The sheer number of these bits of data would overwhelm even the most devoted devotee of the capital markets.

Luckily, the Internet, which has created this problem, also offers a solution – look up the data. Every time one sees a story or conclusion that seems either too good to be true (“Eating Prunes Will Cure Cancer!”) or too sad to be real (“Left-handed People Have Lower Life Expectancies!”), it may be possible to access the data underlying the claim. When one can find the original data upon which the story or conclusion is based (claims without data exist in large numbers, but are usually easier to dismiss), one can often verify or nullify the claim. Sometimes, the data can be read a number of different ways; this too provides the person willing to dig a bit deeper with additional, potentially useful insights.

Just the Facts, Ma’am

In the 1960s television police drama Dragnet, Detective Joe Friday (portrayed by the wonderfully stoic Jack Webb), made famous the line “Just the facts, Ma’am.” As he collected evidence to figure out what happened at a crime scene, he would interview eyewitnesses, but would cut them off with this line when they started offering opinions and conclusions instead of simple facts. Sir Arthur Conan Doyle’s famous character, Sherlock Holmes, was another huge fan of data. Said he, “I never guess. It is a capital mistake to theorize before one has data. Insensibly one begins to twist facts to suit theories, instead of theories to suit facts.” Navigating through the oceans of information now available to us may be akin to assessing a crime scene or solving a murder mystery. There may be lots of information, but determining which bits are important, relevant and/or untainted could greatly help in reaching actionable conclusions.

Often ideas that seem highly intuitive are not supported by the data. For example, it is widely held that in the United States the Republican Party is more pro-business than is the Democratic Party. It would then follow that a Republican President would be good for business in America. This line of logic would lead us to the conclusion that the stock market might benefit more during the tenure of a Republican President than a Democratic one. Let us look at the data. In the 35 years since Jimmy Carter became president, the simple average four-year stock returns during a Republican Presidency was 35.9%. Most investors would welcome this kind of return from stocks. During the Democratic Presidencies, the returns were 62.4%. Are you surprised by these data?

The exact reasons for this surprising disparity are beyond the scope of this essay, but let it suffice to say that the drivers of stock market returns are highly complex and usually defy a simple solution. Key drivers such as business cycles, corporate earnings, interest rates, and so forth may be impacted by Presidential politics at the margin, but are rarely (as the data suggest) the most important factor.

This “look at the facts” approach may lead one to question many intuitive, but ultimately mistaken “givens” in life. Humans seem innately drawn to the easy answer. Unfortunately, the easy answer is often the “wrong” answer as it applies to complex systems such as the capital markets, medicine, science and climatology.

Rarely do we find good reason to quote Roseanne Barr, but the following seems appropriate here. “I like facts and data because they help me think clearly, beyond the cultural messages that I ingest unwittingly, and sometimes find myself regurgitating almost unconsciously.” Most of us are likely guilty at times of “unconsciously regurgitating” an idea or story where we did not check the facts. How many times did our listeners do the same? How often do these “stories” spin on and on until they become considered as bedrock truth? As the American popular science author, Mary Roach, famously penned, “In my experience, the most stanchly held views are based on ignorance or accepted dogma, not carefully considered accumulations of facts. The more you expose the intricacies and realities of the situation, the less clear-cut things become.”

Survey Says…

In the television game show Family Feud, contestants try to guess the most popular answers to a series of surveys. The survey questions cover a broad array of common, everyday topics about which the average person might have a reasonable opinion. “Name something a person might donate to charity” could be a question posed on the show. The key entertainment value of the show (according to most surveys…) are the unpredictable or inane answers the live contestants put forth. If a contestant were to answer “Bowling ball” to the above question, the show’s host would fight a bit of laughter and then show the contestant that his/her answer was not one of the top answers to the survey question. Merriment and mirth usually ensues.

Outside of television game shows, polls and surveys are serious business. Businesses and politicians consider them critical to success. Knowing what “the people” are thinking about any given topic has become a holy grail of sorts to all kinds of policy and business leaders. Although it may be hard to quantify their impact on elections and consumer trends, it would be easy to conclude that the impact is huge.

Surveys are clearly an important form of information, but they are not the same thing as facts. Surveys are subject to factors that can significantly affect their usefulness and/or objectivity. For example, some surveys ask questions with set or fixed answers. Those surveyed must select the answer that most correctly fits their view. The results may not reflect true opinions because perhaps the “true” answer was not one of the ones offered. Some surveys are offered to a targeted set of individuals (college students, for example), but the results could be presented as the opinions of a broader group of individuals. Ultimately, it may be hard to know whether people are honestly answering the questions. Maybe they lack strong opinions. Maybe they are trying to skew the results.

Learning How Not to be Deceived

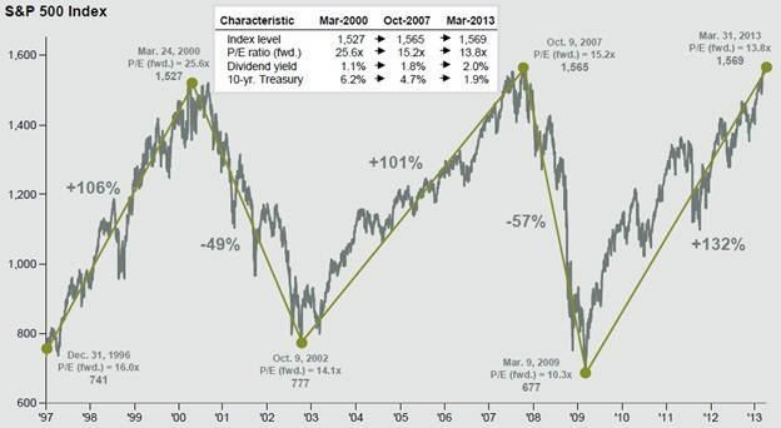

Data are not truth, and the truth may not be provable by data. Yet, much of what we see each day in the media passes itself off as some form of “truth.” As our Chief Investment Officer, Michael Goodson, often says, “There’s nothing more expensive than free advice.” Almost no one offering free investment advice has the well-being of the listener in mind. They may be hawking some proprietary product or service, they may be recommending something to buy that they already own, they may be trying to make a name for themselves by making predictions that might come true, and we cannot discount the possibility that some people just like to hear the sound of their own voice. Trading on this advice might lead to profits some of the time, but over time, it is likely to lead to below-market returns. We see a lot of this every week, and our clients will sometimes send us a copy of one of these articles or emails and ask for our perspective. Here is a good example from this year. Sometime around April, we began seeing emails and articles from people worried that the stock market was about to crash. The chart below was the main reason for this concern.

We read the original report from which this graph was taken, and its actual intent was to show that the market was trading at a much lower P/E value than in 2000 and 2007. The author of the original report was actually arguing that this level does not have to be a peak just because it corresponds to past ones. The emails we saw argued for the exact opposite. The saw-tooth pattern of the chart led some to believe that the market would “have to” go back to the bottom of this pattern, something around 700 or 50% lower than the current price at that time.

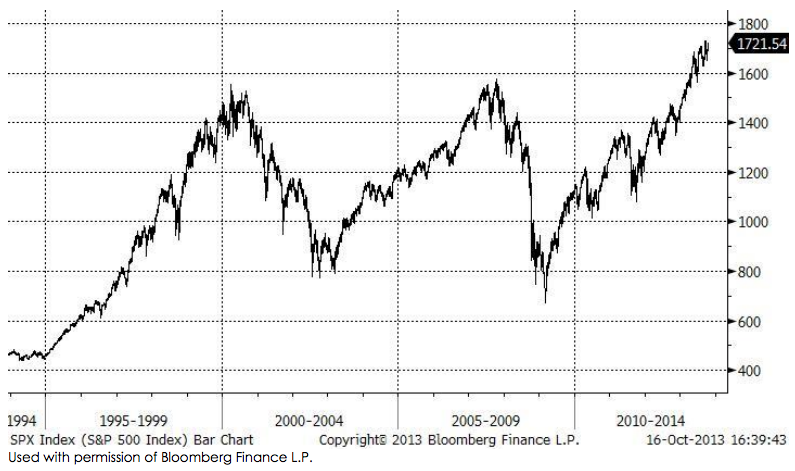

This is where looking at the data could help. Looking at a longer term chart for the S&P 500 (see below), we see that the 800 level for the S&P 500 is nothing special; it is not a magical bottom for the market. We also see that the long-term pattern for the stock market is upward, not saw-toothed. Anyone who traded on this bit of “free” advice might have sold stocks and missed the 10% appreciation since that time. The pattern and the e-mails/articles claiming some useful insights based on the chart proved worse than useless.

Not every blog post or media article is dangerous, just as not every bit of advice is without some merit. The complexity of the investment process requires one to use a broad range of tools and disciplines. The “easy answer,” as intuitively pleasing as it may be, rarely captures the key factors affecting the market at any point in time. When one hears something like, “The key to the market is…” whatever follows should be viewed with a skeptic’s eye. Rarely does one thing drive the market. Rarely does one investment tactic or strategy fit all investors. Looking at the data may not assure one can assess the true nature of all things, but we think the data can provide some context and clarity amid the cacophony of opinions we hear and read each day. As the American economist Emily Oster has said, “The value of having numbers – data – is that they aren’t subject to someone else’s interpretation. They are just numbers. You can decide what they mean for you.”

The Outlook

The 800-pound gorilla in the room at the time of this writing is the so-called “government shutdown” and the on-going debate about raising the U.S. debt ceiling. By the time this letter reaches our clients, we suspect that these issues will be resolved in one way or another, and thus, will no longer be the “big worry” for the market. Absent this bit of melodrama, fundamentals look quite good. The global economy continues to grow, as do corporate earnings. Interest rates are still on the low side, and central banks around the globe are still in easy-money mode. Sentiment has clearly taken a hit from the hijinks in Washington, but a reasonable resolution here could improve sentiment as quickly as it soured.

Yet, there will be a measurable impact to the shutdown. Economists predict that fourth quarter GPD will be negatively impacted by about 15 basis points per week of the shutdown. The heavily-watched jobs report for September was not released due to the shutdown, and this too will likely lead to more uncertainty. The unemployment rate is one of the key components in the Fed’s decision whether to taper the current Quantitative Easing program. Due to the shutdown, a “clean” jobs number will not appear until early December. This means that a decision regarding tapering has likely been pushed all the way back to January at the earliest. So, even when the dickering in Washington has ceased, the markets will still have to deal with some of its lingering effects.

We continue to think that we are in an equity bull market. We would view any weakness due to the wrangling in Washington or the fallout from weaker-thanexpected Q4 economic data, to be a buying opportunity. Cash (beyond some reasonable “rainy day” reserve) continues to be the worst asset to hold for investors, in our view. Doomsday preppers should continue to hold cash, gold and ammo. We continue to think that the longer-term trend for interest rates may be higher, but a simple “sell bonds and buy stocks” cannot apply to all investors. Patches of economic weakness, uncertainty due to military (or political) conflict and market shocks are all good reasons for investors whose long-term asset allocation is not 100% stocks to hold bonds.

Sincerely,

Wolf Group Capital Advisors