It’s been a long time since the words “new normal” were commonly used in the popular media. This term was frequently cited to describe the new era we supposedly entered a while back where the economy would never grow, stocks would never rise again, and basically, life as we knew it would never be the same. As the U.S. economy completes its 13th consecutive quarter of positive economic growth and the stock market celebrates the 42nd month of the current bull market phase, we are led to wonder whatever happened to the new normal? Granted, challenges remain, and not all is perfect in the world (but then, when is it ever perfect, really?). Another way to look at 2012 so far is to consider that the U.S. stock market has provided an aboveaverage annual return (roughly 16%) in only nine months, and it has generated this high return in the face of so much economic and political turmoil (Euro-Crisis, China slowdown, U.S. Presidential election, etc.). There seems to be very resilient and powerful forces at work boosting stock prices. As is usually the case, the reasons for this “unexpected” rise in stock prices are probably the normal suspects – corporate earnings, interest rates, expectations and negative investor sentiment. But what is “normal” anyway? Let’s consider this and other issues after the review.

Third Quarter Review

For the quarter, most stock indices recorded healthy gains, with the broad S&P 500 gaining 6.4%. It’s difficult to pin down one reason for the rise in stock prices, but the announcement that the European Central Bank would begin to buy the debt of some troubled countries there was one likely positive which helped stock prices. The U.S. Fed’s publicly stated intention to hold interest rates low for several years was also a likely positive. Other economic data suggested a dramatic slowdown in the emerging markets, caused by a tightening of monetary policy a few months back. On the positive side, we are seeing encouraging signs of a recovery in the U.S. real estate market. Consumer spending overall has been supportive to economic growth here as well.

Fixed income securities lagged equities in the quarter, but continued to show positive returns as investors are convinced that higher interest rates are unlikely in the face the of the Fed’s pledge to keep short rates low. Retail investors continue to pile into bond funds at a record pace. The data suggest that these investors are moving from cash into bonds, but there is some evidence that they may be selling some equity holdings to fund their bond purchases as well. Despite the positive returns in stocks so far this year, there is little evidence that retail investors are adding to equity exposure.

Here’s what the third quarter looked like by the numbers:

| Index | 3rd Quarter 2012 | Year to Date | Trailing 12 Months |

|---|---|---|---|

| Dow Jones Industrial Average | 5.0% | 10.9% | 26.0% |

| S&P 500 | 6.4% | 16.4% | 30.2% |

| NASDAQ | 6.2% | 19.6% | 29.0% |

| Russell 2000 | 5.3% | 14.2% | 31.9% |

| MSCI EAFE | 6.9% | 10.1% | 13.8% |

| MSCI EAFE Small Cap | 7.9% | 12.4% | 17.6% |

| MSCI Emerging Markets | 7.0% | 9.4% | 13.9% |

| Barclays Aggregate Bond | 1.6% | 4.0% | 5.2% |

| Barclays Municipal Bond | 2.3% | 6.1% | 8.3% |

| Dow Jones Commodities | 10.0% | 4.7% | 5.9% |

A Quick Look at the “Normal”

The word “normal” has a number of connotations. Common synonyms for the word could include “usual,” “common,” “typical” or even “average.” Physiologically speaking, “normal” could mean having all the usual body parts, five fingers, five toes, etc. In this way, “normal” actually means “good.” In math, a normal distribution is one which features perfect symmetry around its mean. Exactly half of the data points are above the mean; the other half falls below it.

In many ways, humans seek to be normal. The opposite of “normal” is “abnormal,” and no sane person would seek that tag. Yet somewhere along the line in our competitive, achievement-oriented world, “normal” has come to suggest “average,” that is to say, not great, not exceptional and, in a way, undesirable. Much like Garrison Keillor’s famous “Lake Wobegon” community, we would like to think that our children (or personal attributes even) are all above average. Alas, most of us (like all data points) cluster around the mean.

Sure, we may know someone at the “tails” of this distribution, but most of the people we interact with on a daily basis are likely fall into the middle part of the distribution. Anyone who might have been teased as a youngster due to being “too tall” or “too short” (interesting how the bulk of the distribution will sometimes denigrate those at either end of the distribution…), can appreciate the concept of falling outside the “norm.”

Most of us would like to be in the right-hand tail of this distribution. Here too, the “tails” are small, and only a few of us will ever be at the extremes of most distributions. In most cases being “normal” is fine. In the U.S., being near the mean of most distributions suggests a life that is comfortable and fulfilling (especially compared to the means we find globally). So while in some things we may wish to be something different, in most cases being “normal” is probably a good thing.

Everybody Loves a Winner

A comprehensive list of “normal” behavior is well beyond the scope of this essay, but one important behavior of “normal” people is cheering for the winner. We all like it when our team wins. Whether in sports, politics, business, the military, or other areas of competition, we like winners. Even people with only passing interest in some area (sports, for example), may find great pleasure in cheering for a winning team in the Olympics, World Cup or World Series.

We also tend to like events where the winner can be easily identified. Elections, car races, sporting matches, and so on are satisfying to the normal person exactly because the end result (winners and losers) can be easily identified. We generally dislike ambiguous outcomes, like contested elections, tie games or really long term issues like the discussions about global climate change. We like to know who won, and we enjoy the endorphin rush of having picked the winner.

This behavior is well reinforced in many aspects of our lives. If we hire someone to work on our house, we expect to have it done right. We have a certain expectation, and when that expectation is fulfilled, we feel like we have won. The outcome is certain, and our expectations were met. We are rightfully disappointed when the outcome is less than we expected. The reputation of the service provider will suffer in our eyes and we may even judge the person harshly in ways not directly linked to the quality of the service performed.

In a similar fashion, when a winning team or person hits a “losing streak,” many of us may change our views of this erstwhile winner. Even though the essence that made that team or person a winner may not have changed, recent results may skew our opinions in potentially illogical ways. We are sometimes quick to tear down the banners celebrating last year’s winner when this performance is not replicated.

Some observers may be critical of this behavior, perhaps in part because it is solely focused on the results and not the essence of the performer. We would disagree, and suggest that cheering for the winner and eschewing the loser is simply “normal” behavior.

How Normal People Invest

Normal people probably approach investing in a similar way to how they pick a plumber. We hear something good about a plumber via a friend, some service or maybe an ad in a newspaper or on television. We have a need (fix a leak, for example), and we hire the person to do the job. If the outcome is favorable (no leak), we are happy to pay and may provide a positive review or tell our friends about the good service. At this point, we really know very little about the plumber, except that he fixed the leak. Maybe he is a very shady businessman. Perhaps he used bubble gum for the repair, and the leak will soon return (just after your check clears). Our opinion of the plumber as a “winner” is based solely on past results.

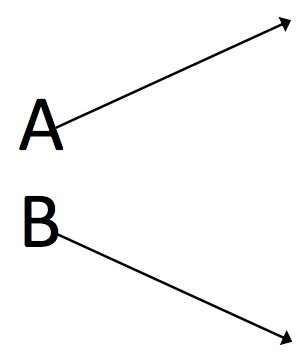

Normal people probably look at a stock (or any investable asset) in a similar way. They might do some research, talk to friends and family and then make the selection with certain expectations (i.e. the asset appreciates). Let’s say an investor invests in two things, “A” and “B,” with the goal of making money. After some period of time, these assets have performed as shown below.

What will a normal person conclude from this? Asset “A” is a winner (because it has gone up), and “B” is a loser (it did not do its job as an investment because it went down). At this point, the investor may know very little about true nature of these assets or their intrinsic value. What is the normal response to this outcome? We would submit that most people would want to sell “B” and buy more of “A.” Why? Because they are normal! Almost everything else in our life experience teaches us that this is a reasonable and perhaps correct approach.

[Aside: if you do not reach the conclusions presented above, you may be “abnormal.” There is no reason to worry; you just may be showing some tendencies normally associated with professional investors. Please refer to the next section for more details.]

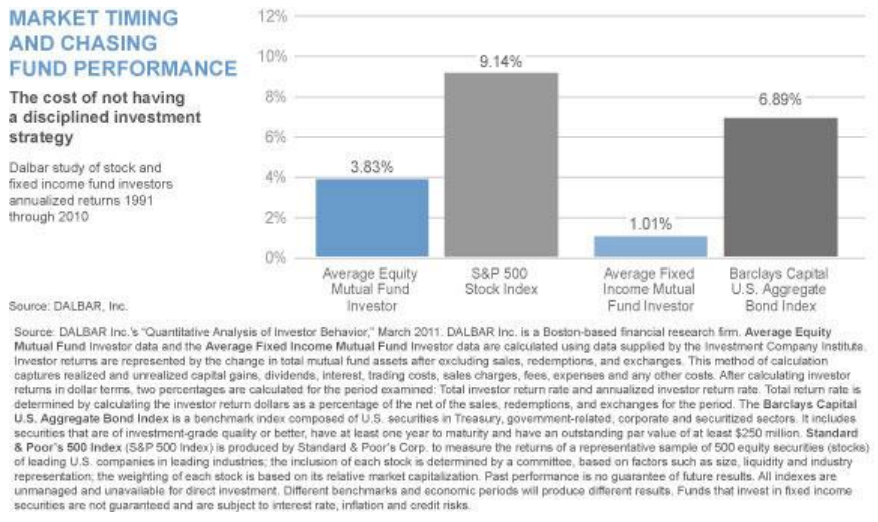

Interestingly, this approach is quite often wrong for investing. Sure, sometimes “B” continues to go down and sometimes “A” continues to go up, but in principle, “B” should be cheaper than “A” and thus may be the better investment at that point in time. Doing the “normal” thing may explain why the “average” retail investor (again, think of this in terms of the normal distribution), achieves much lower than index returns. The chart on the next page illustrates this tendency.

In practice, the “normal” investor will tend to “buy high and sell low.” They will buy a stock or an asset after it has appreciated (like “A”), and then impute to it all kinds of virtue solely by its price appreciation. This behavior was rampant in the tech bubble in the 1990s. They will sell low for the same reason. This behavior was widespread in the financial crisis in 2008 and 2009. We still hear about people who sold during that time and have remained in cash waiting for “things to settle down.” Meanwhile, the stock market has risen well over 100% from the March 2009 lows.

Why do we do this? It is in large part because most people lack the time, temperament and/or talent to be successful investors. A person who really wants to improve his or her investment prowess can dedicate the time and acquire the talent through study, research and training. This leaves temperament as the missing ingredient. To constantly go against the flow of the crowd is a mindset not easily acquired. The ability to see the potential treasure in another’s trash can is not a common trait. We all may think we have this temperament, but our actions in times of stress (say, March of 2009) will speak to our true nature in this regard.

How Professional Investors (aka “Abnormal People”) Invest

Most professional investors deploy a disciplined investment strategy to be successful. They have been trained by experience in the market to look well beyond the price action of an asset. [Aside: There are many investors who use short-term trading techniques which rely heavily on price movements and technical metrics. They are a breed apart from the professional investors to whom we are referring]. Investors with a disciplined strategy will spend a great deal of effort understanding the nature of the asset, attempt to measure its intrinsic value, create various scenarios under which the asset can provide attractive returns, then try to determine where the asset is trading relative to their estimates. In this way, asset “B” may be more interesting to the professional investor, assuming that “A” and “B” are similar in nature. But the key point here is that the professional investor will look beyond just the “story” of the investment or its price chart to determine how to proceed.

There are very few certainties in the investment world. Sometimes an asset that looked like junk to normal people and a possible treasure to professional investors turns out to be junk! When that happens, the professional investors can learn from the mistake, reassess the methodology/measuring techniques and move forward. Sometimes when an individual investor is losing money in an asset they will brand it a “loser” and avoid it from then on, regardless of any future potential it may have.

If investing profitably were easy, everyone would do it. If it were comfortably intuitive, everyone would want to do it. The reality is that investing successfully takes a certain mindset that seems to be at odds with “normal” thinking. This is not to suggest that professional investors are all “abnormal,” but many of them (by their own admission) are. But this is perhaps as it should be. Firefighters may be considered “abnormal” because they run into burning buildings versus the “normal” person who would run out. Maybe all of us have something special about us that moves us a ways from the mean of some distribution or other. Maybe this is why the world is such a diverse and interesting place…

What can you take away from this other than it is an interesting discussion? We would argue that if you are more aware of these types of “normal” tendencies, you will be more mindful of the opportunities that arise, and better able to make informed decisions without the emotions that may lead to poor decisions.

The Outlook

Our view remains mostly unchanged from our last report. We continue to think we are in a bull market for stocks and close to a peak in bond prices. Cash continues to be the most dangerous asset/investment to hold, in our view.

If anything, we are a bit more bullish on stocks than before. It seems that some investors may be holding back due to fear about the economy, the so-called “fiscal cliff” issues, Europe, and the U.S. presidential elections. In light of the recent data regarding housing and employment, we feel a bit more optimistic about the outlook for 2013. Europe will continue to be a drag on the global economy, but not forever. Any good on that front would likely be embraced by the markets warmly. The uncertainties about the “fiscal cliff” and the election will likely be mostly resolved after November 6th. We suspect that Congressional leaders already have some kind of compromise plan in the works and are only waiting to see who will be the president. No politician would want to cause an unnecessary recession by their unwillingness to act in a mature and sensible way. The resolutions of these uncertainties coupled with better economic data could help move stocks even higher.

We think that the emerging market economies are likely to rebound over the next 6 to 12 months as well. Monetary easing usually has a bigger impact on these economies, and their central banks have been easing for a few quarters. We can create reasonable scenarios where many positives line up in ways not seen for a long time.

As usual, we don’t know for sure what’s going to happen over the next 6 months or 12 months. We do know that many stocks are trading at attractive discounts to their fair value. We also know that equities have always afforded the best returns of any asset class over time. As the “new normal” fades away into the graveyard of overused and misused phrases, we are left to wonder if the new reality is perhaps very similar to the norms in decades past – stocks continue to offer the greatest upside potential of all the major asset classes… Time will tell.

Sincerely,

Wolf Group Capital Advisors